Pharmacies Pull Zantac Over Concern That Contaminant Poses Cancer Risk

Major U.S. pharmacies have pulled Zantac and its generic equivalent off the shelves after concern about a contaminant that poses a small cancer risk.

Major U.S. pharmacies have pulled Zantac and its generic equivalent off the shelves after concern about a contaminant that poses a small cancer risk.

Missouri resident Patricia Powers had no health insurance when she was diagnosed with cancer a few years ago; she and her disabled husband were struggling to get by on, at most, $1,500 a month. If they’d lived across the river in Illinois, she’d have been eligible for Medicaid.

Laura Ungar/Kaiser Health News

hide caption

toggle caption

Laura Ungar/Kaiser Health News

Patricia Powers went a few years without health insurance and was unable to afford regular doctor visits. So the Missouri resident, who lives near St. Louis, had no idea cancerous tumors were silently growing in both of her breasts.

If Powers lived just across the Mississippi River in neighboring Illinois, she would have qualified for Medicaid, the federal-state health insurance program for low-income residents that 36 states and the District of Columbia decided to expand under the Affordable Care Act. But Missouri politicians chose not to expand it — a decision some groups are trying to reverse by getting signatures to put the option on the 2020 ballot.

Powers’ predicament reflects an odd twist in the way the health care law has played out: State borders have become arbitrary dividing lines between Medicaid’s haves and have-nots, with Americans in similar financial straits facing vastly different health care fortunes. This affects everything from whether diseases are caught early to whether people can stay well enough to work.

It wasn’t supposed to be this way. The ACA, passed in 2010, called for extending Medicaid to all Americans earning up to 138% of the federal poverty level, around $17,000 annually for an individual. But the U.S. Supreme Court in 2012 let states choose whether to expand Medicaid. Illinois did, bringing an additional 650,000-plus people onto its rolls. Missouri did not, and today about 200,000 of its residents are like Powers, stuck in this geographic gap.

Powers, who was in her early 60s when diagnosed with cancer, had briefly thought about moving to another state, just to be able to get Medicaid. “You ask yourself: Where do you go? What do you do?” says Powers. “Do I look at what’s happening in Illinois, right across the river?”

A recent University of Michigan study found Medicaid expansion substantially reduced mortality rates from 2014 to 2017. The researchers said Illinois averted 345 deaths annually while Missouri had 194 additional deaths each year. The same trends held for other side-by-side states such as Kentucky (did expand) and Tennessee (did not), New Mexico (did) and Texas (did not).

Dr. Karen Joynt Maddox, co-director of the Center for Health Economics and Policy at Washington University in St. Louis, says health care providers in her border city see how the coverage differences affect people. When treating Medicaid patients from Illinois, she says, doctors know procedures, equipment and medicines will likely be covered. With uninsured Missourians, they must consider whether patients can afford even follow-up medications after heart attacks.

Nonetheless, Medicaid expansion faces significant opposition in Missouri, which is a red state — led by a Republican governor with GOP supermajorities in both legislative chambers.

Patrick Ishmael, director of government accountability for the Show-Me Institute, a Missouri free-market think tank, says offering Medicaid to people with incomes above the poverty level would drain resources from the state’s underserved poor and push up taxpayer costs. Though the federal government pays 90% of the cost of the expansion coverage, he says, Missourians contribute to that through their federal taxes. Medicaid already accounts for about a third of the state’s budget, which he says puts pressure on other priorities, like education.

“Missouri and other states need to think about whether they are a government that provides health care or a health care provider that sometimes governs,” he says.

A Missouri story

Powers, a minister in the St. Louis County suburb of Hazelwood, used to get health insurance through her husband’s job selling lumber and hardware. After he was disabled in 2009, their coverage continued on and off for a while, and her husband eventually received Medicare, the federal insurance program for people who are 65 and older or who have disabilities. But Powers had no insurance starting in 2012 as the couple struggled on, at most, $1,500 a month.

Medicaid wasn’t an option for her. Missouri could have opened the program to more adults as early as 2010, in preparation for the health care law’s expanded coverage taking effect in 2014. Without the ACA’s expansion, adults who aren’t 65-or-older or disabled don’t qualify, no matter how low their income. Missouri’s program generally covers only pregnant women and children from low-income families, and people who are poor and elderly, blind or disabled.

Powers and her husband earned too little for her to qualify for subsidies on the federal ACA marketplace, so she couldn’t afford to buy her own plan. And without insurance, Powers never saw doctors for routine health visits or screenings. She stopped taking her prescribed medications for high blood pressure and anxiety — until she could no longer do without the anti-anxiety medicine, Lexapro.

In early 2016, she discovered a place to get help when she gave her friend a ride to a St. Louis clinic for the uninsured called Casa de Salud, where health services cost less than $30.

Powers figured she’d ask about getting back onto Lexapro there. She got a thorough checkup. The doctor found a walnut-sized lump in her right breast, and a mammogram found a tumor the size of a grain of rice in her left.

A clinic caseworker helped Powers sign up for a Medicaid program for breast cancer patients. She underwent surgery in April 2016, then had 35 radiation treatments and took follow-up medications.

Powers kept thinking she could have found the cancer earlier, if only she had insurance. That would have meant less treatment and lower costs for taxpayers, who ended up footing the bill anyway. Research shows breast cancer in its earliest stage can cost half as much to treat as in later stages.

“Even if you didn’t care about the human cost, you should care about the economic cost,” says Jorge Riopedre, president and CEO of Casa de Salud. “Treating a disease at its first stage is always going to be much cheaper than treating it at its advanced stage.”

An Illinois story

In neighboring Illinois, getting Medicaid through the expansion helped Matt Bednarowicz avoid debilitating medical debt after a motorcycle crash.

The wreck crushed his left foot, requiring doctors to insert pins in it. Without Medicaid, he would have faced thousands of dollars in medical bills.

“The debt would have been greater than I could comprehend overcoming,” says Bednarowicz, who is now 29.

His Medicaid kicked in “just in the nick of time” to cover the surgery, Bednarowicz says. It also allowed him to get psychiatric help for depression. More than a year later, he’s able to get around well — even jog — and works as a caregiver for an elderly man.

Having insurance helps people like Bednarowicz stay productive, says Riopedre.

“The person who gets sick can’t work, can’t support his or her family, can’t be a consumer and buy goods. If they’re not working, they can’t pay taxes,” Riopedre says. “It just is a tidal wave of downstream effects that if we can’t get it right — it’s going to have repercussions across the nation.”

Amid controversy, future uncertain for Missouri

As the ballot measure push continues, Missouri Gov. Mike Parson, a Republican, recently created a task force to look into expanding Medicaid through a waiver allowing states to skip some federal requirements. His office referred questions to the state’s Department of Health and Senior Services, which in turn referred them to the Department of Social Services. Rebecca Woelfel, a spokeswoman for that agency, says the department doesn’t typically comment on potential ballot issues.

Ishmael, of the Show-Me Institute, says he hopes the push for expansion doesn’t get that far. He says the Medicaid system overall is wasteful, with outcomes often not fully justifying the expense. The cost of an expansion would depend on how it’s structured, he says, but “it could be a real budget-buster.”

The impact of an expansion on Missouri’s budget remains unclear. A February analysis by researchers at Washington University estimated it would be “approximately revenue-neutral.” But their estimates range widely for the first year depending on enrollment and other factors, from up to $95 million in savings for Missouri’s Medicaid program to costing $42 million more than not expanding.

Powers, whose husband died last year, says she fully supports Medicaid expansion.

But whatever happens, especially now that she’s suffering from heart failure, she’s grateful she won’t have to worry about being uninsured again. At 66, she’s now old enough for Medicare.

Kaiser Health News is a nonprofit, editorially independent program of the Kaiser Family Foundation. KHN is not affiliated with Kaiser Permanente.

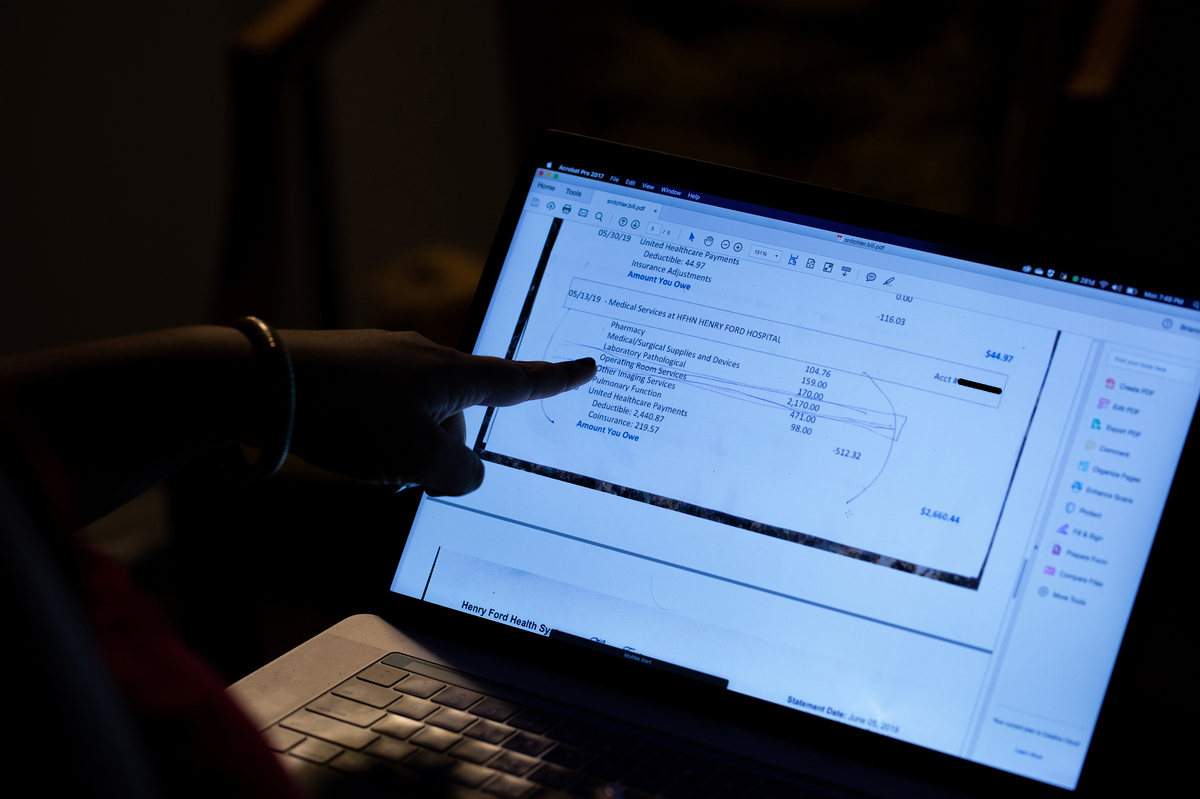

An unexpected charge related to a biopsy threatened the financial security of Brianna Snitchler and her partner.

Callie Richmond for Kaiser Health News

hide caption

toggle caption

Callie Richmond for Kaiser Health News

Brianna Snitchler was just figuring out the art of adulting when she scheduled a biopsy at Henry Ford Hospital in Detroit.

Snitchler, 27, was on top of her finances: Her student loan balance was down and her credit score was up.

“I had been working for the past three years trying to improve my credit and, you know, just become a functioning adult human being,” Snitchler said.

For the first time in her adult life, she had health insurance through her job and a primary care doctor she liked. Together they were working on Snitchler’s concerns about her mental and physical health.

One concern was a cyst on her abdomen. The growth was about the size of a quarter, and it didn’t hurt or particularly worry Snitchler. But it did make her self-conscious whenever she went for a swim.

“People would always call it out and be alarmed by it,” she recalled.

Share Your Story And Bill With Us

If you’ve had a medical-billing experience that you think we should investigate, you can share the bill and describe what happened here.

Before having the cyst removed, Snitchler’s doctor wanted to check the growth for cancer. After a first round of screening tests, Snitchler had an ultrasound-guided needle biopsy at the Henry Ford Health System’s main hospital.

The procedure was “uneventful,” with no complications reported, according to results faxed to her primary care doctor after the procedure. The growth was indeed benign, and Snitchler thought her next step would be getting the cyst removed.

Then the bill came.

The patient: Brianna Snitchler, 27, a user-experience designer living in Detroit at the time. As a contractor for Ford Motor Co., she had a UnitedHealth Group insurance plan.

Total bill: $3,357.52, including a $2,170 facility fee listed as “operating room services.” The balance included a biopsy, ultrasound, physician charges and lab tests.

Service provider: Henry Ford Health System in Detroit.

Medical procedure: Ultrasound-guided needle biopsy of a cyst.

What gives: When Snitchler scheduled the biopsy, no one told her that Henry Ford Health System would also charge her a $2,170 facility fee.

Snitchler said the bill turned out to be far more than what she had budgeted for. Her insurance plan from UnitedHealth had a high deductible of $3,250, plus she would owe coinsurance. All told, her bills for the care she received related to the biopsy left her on the hook for $3,357.52, with her insurance paying $974.

When Brianna Snitchler scheduled the biopsy for a cyst on her abdomen, no one told her that the Henry Ford Health System would charge a $2,170 facility fee, listed on her bill as “operating room services.” (Note: This photo has been edited to redact private information.)

Callie Richmond for Kaiser Health News

hide caption

toggle caption

Callie Richmond for Kaiser Health News

“She shrugged it off,” Snitchler’s partner, Emi Aguilar, recalled. “But I could see that she was upset in her eyes.”

Snitchler panicked when she realized the bill threatened the couple’s financial security. Snitchler had already spent down her savings for a recent cross-country move to Austin, Texas.

In an email, Henry Ford spokesman David Olejarz said the “procedure was performed in the Interventional Radiology procedure room, where the imaging allows the biopsy to be much more precise.”

“We perform procedures in the most appropriate venue to ensure the highest standards of patient quality and safety,” Olejarz wrote.

The initial bill from Henry Ford referred to “operating room services.” The hospital later sent an itemized bill that referred to the charge for a treatment room in the radiology department. Both descriptions boil down to a facility fee, a common charge that has become controversial as hospitals search for additional streams of income, and as more patients complain they’ve been blindsided by these fees.

Hospital officials argue that medical centers need the boosted income to provide the expensive care sick patients require, 24 hours a day, 365 days a year.

But the way hospitals calculate facility fees is “a black box,” said Ted Doolittle, with the Office of the Healthcare Advocate for Connecticut, a state that has put a spotlight on the issue.

“It’s somewhat akin to a cover charge” at a club, said Doolittle, who previously served as deputy director of the federal Center for Program Integrity at the Centers for Medicare & Medicaid Services.

Hospitals in Connecticut billed more than $1 billion in facility fees in 2015 and 2016, according to state records. In 2015, Connecticut lawmakers approved a bill that forces all hospitals and medical providers to disclose facility fees upfront. Now patients in Connecticut “should never be charged a facility fee without being shown in burning scarlet letters that they are going to get charged this fee,” Doolittle said.

In Michigan, there’s no law requiring hospitals and other providers of health care services to inform patients of facility fees ahead of time.

Snitchler’s procedure took place on campus at Henry Ford’s main hospital site. When she got her bill, with its mention of “operating room services,” she was baffled. Snitchler said the room had “crazy medical equipment,” but she was still in her street clothes as a nurse numbed her cyst, and she was sent home in a matter of minutes.

With Snitchler’s permission, Kaiser Health News shared her itemized bill, biopsy results and explanation of benefits with Mark Weiss, a radiologist who leads MediCrew, a company in Flint, Mich., that helps patients navigate the health system.

Weiss said it probably wasn’t medically necessary for Snitchler to go to the hospital to receive good care. “Not all surgical procedures have to be done at a surgical center,” he said, noting that biopsies often can be done in an office-based treatment center.

Resolution: Hoping for a reasonable explanation — or even the discovery of a mistake — Snitchler called her insurance company and the hospital.

A representative at Henry Ford told her on the phone that the hospital isn’t “legally required” to inform patients of fees ahead of time.

In an email, Henry Ford spokesman Olejarz apologized for that response: “We’ll use it as a teachable moment for our staff. We are committed to being transparent with our patients about what we charge.”

He pointed to an initiative launched in 2018 that helps patients anticipate out-of-pocket expenses. The program targets the most common elective radiology and gastroenterology tests that often have high price tags for patients.

Asked if Snitchler’s ultrasound-guided needle biopsy will be included in the price transparency initiative, Olejarz replied, “Can’t say at this point.”

In addition to the pilot program to inform patients of fees, Olejarz said, the hospital also plans to roll out an online cost-estimator tool.

For now, Snitchler has decided not to get the cyst removed, and she plans to try to negotiate on her bill. She has not yet paid any portion of it.

“You should always negotiate; you should always try,” Doolittle said. “Doesn’t mean it’s going to work, but it can work. People should not be shy about it.”

“We are happy to work out a flexible payment plan that best meets her needs,” Olejarz wrote when Kaiser Health News first inquired about Snitchler’s bill.

The takeaway: When your doctor recommends an outpatient test or procedure like a biopsy, be aware that the hospital may be the most expensive place you can have it done. Ask your physician for recommendations of where else you might have the procedure, and then call each facility to try to get an estimate of the costs you’d face.

Also, be wary of places that may look like independent doctor’s offices but are owned by a hospital. These practices also can tack hefty facility fees onto your bill.

If you get a bill that seems inflated, call your hospital and insurer and try to negotiate it down.

Bill of the Month is a crowdsourced investigation by Kaiser Health News and NPR that dissects and explains medical bills. Do you have an interesting medical bill you want to share with us? Tell us about it!

A key issue in the contract dispute between General Motors and the United Auto Workers is health benefits. Workers have had famously great health plans, paying just 3% of costs.

SCOTT SIMON, HOST:

The United Auto Workers strike of about 50,000 General Motors workers is about to enter its third week. A key issue in the contract dispute is health benefits. The company argues that it cannot shoulder rising health costs. Union members want to hang onto their famously great health plans. Workers mostly pay no premiums, $25 for a doctor’s visit and just a few dollars for prescriptions. NPR’s Selena Simmons-Duffin wondered how’d they get those plans.

SELENA SIMMONS-DUFFIN, BYLINE: To answer that question, let’s go back to 1950. The country had just made it through the Depression, two world wars…

ERIK LOOMIS: By 1950, the economy is pretty much booming.

SIMMONS-DUFFIN: Erik Loomis is a history professor at the University of Rhode Island.

LOOMIS: It creates a massive consumer market for a lot of products in the United States, very much including automobiles.

(SOUNDBITE OF ARCHIVED RECORDING)

UNIDENTIFIED PERSON #1: More and more people are driving this car and buying this car.

SIMMONS-DUFFIN: Automakers were scrambling to meet the demand, but they had to bargain with the unionized workforce. The UAW was well-organized, had connections in high places. And what it wanted to get with this leverage was a role in automakers decisions – how many workers to hire, what kind of cars to make, whether to keep factories open.

LOOMIS: And the companies totally resisted this.

SIMMONS-DUFFIN: So the UAW called lots of strikes, which were costly. Finally in 1950, a historic agreement.

LOOMIS: The Treaty of Detroit. And that is a compromise between the UAW and the Big Three automakers that basically says that the UAW will give up its demands to open company books and have control over production decisions. In exchange for that, the workers themselves will get massive wage increases and significant benefit packages.

SIMMONS-DUFFIN: One of those benefits, health insurance, which was kind of a new-fangled idea. Medical care was just starting to be something that might cure you and cost you. Insurers were cropping up saying, hey, why not pay a little at a time instead of all at once.

(SOUNDBITE OF ARCHIVED RECORDING)

UNIDENTIFIED PERSON #2: What I don’t worry about is our health care. We’ve joined Cigna Health Plan.

SIMMONS-DUFFIN: These benefits were actually a good deal for employers. There were tax advantages. More and more companies began to offer health plans to their employees. And union autoworkers, with their benefits, got back to building cars.

(SOUNDBITE OF ARCHIVED RECORDING)

UNIDENTIFIED PERSON #3: Modern assembly is timing and teamwork as well as organization.

SIMMONS-DUFFIN: Loomis says back in the 1960s, the idea of a company covering the full cost of health benefits wasn’t that unusual.

LOOMIS: You don’t really see workers have to begin to cover large chunks of their health care until the 1980s.

SIMMONS-DUFFIN: The incredible thing is that the UAW hung on to their low-cost benefits as the rest of us began to pay more and more. Today, workers on employee plans pay about 30% of their health care costs. UAW workers pay about 3%. Not that it’s been easy for the unions, says Kristin Dziczek. She’s vice president of the Center for Automotive Research.

Is it a struggle in every contract negotiation or is it…

KRISTIN DZICZEK: Yes, absolutely. Every time this is a big struggle.

SIMMONS-DUFFIN: Especially as health care costs have gone up for everyone. Dziczek says today GM and other automakers argue the cost of these health benefits is unsustainable. GM told NPR it cost $900 million in 2018.

DZICZEK: The impression is that the employer is paying. But in reality, the employees, the union is paying here as well because the increasing costs of medical care and benefits is eating into their ability to get wage or other benefit gains. It eats up a bigger and bigger share of the amount of money that’s on the table.

SIMMONS-DUFFIN: Even if this time the union manages to preserve their enviable health benefits, next time the contract is up, they’ll have to fight to keep them once again. Selena Simmons-Duffin, NPR News.

Copyright © 2019 NPR. All rights reserved. Visit our website terms of use and permissions pages at www.npr.org for further information.

NPR transcripts are created on a rush deadline by Verb8tm, Inc., an NPR contractor, and produced using a proprietary transcription process developed with NPR. This text may not be in its final form and may be updated or revised in the future. Accuracy and availability may vary. The authoritative record of NPR’s programming is the audio record.

In the alleged scheme, Medicare beneficiaries were offered, at no cost to them, genetic testing to estimate their cancer risk.

Al Drago/Bloomberg/Getty Images

hide caption

toggle caption

Al Drago/Bloomberg/Getty Images

In announcing a crackdown Friday on companies it says were involved in fraudulent genetic testing, the U.S. Department of Justice brought charges against 35 individuals associated with dozens of telemarketing companies and testing labs.

The federal investigation, called Operation Double Helix, went after schemes that allegedly targeted people 65 and older. According to the charges, the schemes involved laboratories paying illegal kickbacks and bribes to medical professionals who were working with fraudulent telemarketers, in exchange for the referral of Medicare beneficiaries.

DOJ officials say the schemes cost the Medicare program more than $2 billion in unnecessary charges.

Among those charged were 10 medical professionals, including nine doctors.

“The elderly and disabled are being preyed upon,” says Joe Beemsterboer, senior deputy chief of the fraud section in the criminal division of the DOJ.

It was one of the largest health care fraud schemes in U.S. history, Beemsterboer, says, and it worked on many levels, involving many players — from “those collecting patient information, to those selling it, to those doctors corruptly prescribing these genetic tests, to the labs corruptly billing the Medicare program.”

According to Shimon Richmond, assistant Inspector General for investigations with the U.S. Department of Health and Human Services, this is how the alleged scheme worked: First, telemarketing companies trolled elderly Medicare beneficiaries online, or called them on the phone or even sent people to approach beneficiaries face-to-face at health fairs, senior centers, low-income housing areas or religious institutions like churches and synagogues.

Seniors were offered, at no cost to them, genetic testing to estimate their cancer risk or determine how well certain drugs would work for them. All they had to do, the elderly people were told, was provide their Medicare information, a copy of their driver’s license and a bit of DNA collected from a swab of saliva from inside their cheek.

The sales pitch also included lots of aggressive scare tactics, Richmond says, such as telling patients that if they didn’t have the testing done they could end up suffering from a variety of possibly fatal conditions.

Once recruiters got the information they wanted, they would try to get the patient’s own health care provider to write a prescription for the test. If that didn’t work, the recruiters asked one of their own cadre of doctors to write prescriptions for patients they didn’t know.

“And these doctors, in many cases, have zero contact with the patient and no knowledge of their health care situation or needs,” Richmond says.

The genetic test may have been offered free to the patients, but there was money to be made from Medicare reimbursement. Typically that payment – anywhere from $10,000 to $18,000 or more, Richmond says — would be split between the worker who recruited the patient, the doctor writing the prescription, the lab that did the test and the telemarketing company that organized the alleged scheme.

Often, the labs didn’t even send results to patients, Richmond says. And when they did there was no counseling or help interpreting the findings.

“So patients were left with a report that’s meaningless to them, and is certainly not providing them with any benefit in terms of their health care,” says Richmond.

The testing could also financially harm the patient down the road, he adds. For example, if, in the future, the patient’s legitimate doctor determines that the patient actually needs a genetic test for a certain condition, Medicare likely won’t cover it, citing an earlier payment.

The U.S. Department of Health and Human Services Office of Inspector General has previously issued a fraud alert for consumers in an effort to educate the public about such schemes.

Richmond says people who believe they may have been victimized by the schemes can call 1-800-HHS-TIPS, or they can file a complaint online.

If convicted, the defendants arrested Friday could face decades in prison, Beemsterboer says.

Health officials say people with vaping-related illness have used more than 200 products sold under 87 brands. That’s complicating efforts to identify the substances contributing to lung damage.

The Justice Department has charged 35 individuals with defrauding Medicare of more than $2 billion. The scheme allegedly involved bribes and kickbacks for genetic tests to predict cancer.

Medicare Advantage health plans, mostly run by private insurance companies, have enrolled more than 22 million seniors and people with disabilities — more than 1 in 3 people who are on some sort of Medicare plan.

Pablo Martinez Monsivais/AP

hide caption

toggle caption

Pablo Martinez Monsivais/AP

Kaiser Health News is suing the U.S. Centers for Medicare & Medicaid Services to release dozens of audits that the agency says reveal hundreds of millions of dollars in overcharges by Medicare Advantage health plans.

The lawsuit filed late Thursday in U.S. District Court in San Francisco under the Freedom of Information Act, seeks copies of 90 government audits of Medicare Advantage health plans conducted for 2011, 2012 and 2013 but never made public. CMS officials have said they expect to collect $650 million in overpayments from the audits. Although the agency has disclosed the names of the several dozen health plans under scrutiny, it has not released any other details.

“This action is about accountability for hundreds of millions of public dollars misspent,” says Elisabeth Rosenthal, KHN’s editor-in-chief. “The public deserves details about the overpayments, since many of these private companies are presumably still providing services to patients and we need to make sure it can’t happen again.”

Medicare Advantage, mostly run by private insurance companies, has enrolled more than 22 million seniors and people with disabilities — more than 1 in 3 people on Medicare.

On July 3, KHN reporters filed a FOIA request that seeks copies of the CMS audits, which are known as Risk Adjustment Data Validation, or RADV, and include the audit spreadsheets, payment error calculations and other records. CMS has yet to respond to that request, according to the lawsuit.

“By this FOIA action, KHN seeks to shine a public light on CMS’s activities on behalf of millions of Americans and their families,” the legal suit states. The suit asks the court to find that CMS violated the FOIA law and order the agency to “immediately disclose the requested records.”

While Medicare publicly discloses audits of other medical businesses, Medicare Advantage insurers “are being treated differently,” according to the suit. “These audits are improperly being withheld by CMS, even though CMS estimates that these audits have identified some $650 million in improper charges,” the lawsuit alleges.

While proving popular with seniors, the Medicare Advantage industry has long faced criticism that it overcharges the government by billions of dollars every year.

Medicare pays the health plans higher rates for sicker patients and less for those in good health. However, the RADV audits have shown that health plans often cannot document whether many patients actually had the medical conditions the government paid them to treat, generating overpayments. The secretive RADV audits are the primary means for CMS to hold the industry accountable and claw back overcharges for the U.S. Treasury.

In July, Kaiser Health News and NPR reported that Medicare Advantage plans have overcharged the government by nearly $30 billion in the past three years alone — money federal officials have struggled to recoup.

This month, U.S. Sen. Sherrod Brown, an Ohio Democrat, and five other senators sent a letter to CMS Administrator Seema Verma asking her to investigate Medicare Advantage overbilling. “In many cases, CMS has known for years about the tendency for some MA plans to overbill the government yet, despite this, CMS has taken little to no action to course correct. It is critical that CMS act immediately to recoup these overpayments and prevent future overbilling by MA plans,” Brown wrote.

The insurance industry is fighting a proposal by CMS that would expand the impact of RADV by extrapolating error rates found in a random sample of patients to the plan’s full membership — a technique expected to trigger many multimillion-dollar penalties.

America’s Health Insurance Plans, the industry’s trade association, issued a written statement on Aug. 28 that said the CMS proposals “violate numerous statutory requirements and are fundamentally unfair and ill-conceived.”

Stepping up RADV penalties “could lead to higher costs, reduced benefits, and fewer MA plan options for seniors,” the group argued.

The FOIA lawsuit is the second by a media organization to compel CMS to disclose RADV audit findings. In 2014, the Center for Public Integrity sued CMS and won a court order forcing release of RADV audits for the first time. The audits showed that 35 of 37 plans had been overpaid, in some cases by as much as $10,000 per patient in a year.

Kaiser Health News is a nonprofit, editorially independent program of the Kaiser Family Foundation. KHN is not affiliated with Kaiser Permanente.

While the United Auto Workers strike continues, General Motors and the union are telling different stories about what’s going on with the health benefits of striking workers and their families.

Some insurers using this new payment model offer a single fee to one OB-GYN or medical practice, which then uses part of that money to cover the hospital care involved in labor and delivery. Other insurers opt to cut a separate contract with the hospital.

Adene Sanchez/Getty Images

hide caption

toggle caption

Adene Sanchez/Getty Images

The thrill of delivering newborns helped pull Dr. Jack Feltz into the field of obstetrics and gynecology.

More than 30 years later, he still enjoys treating patients, he says. But now Feltz is also working to change the way doctors are paid for maternity care.

Feltz’s New Jersey-based practice, Lifeline Medical Associates, recently partnered with the insurer UnitedHealthcare to test a new payment model. The insurer sets a budget with the practice to pay doctors one lump sum for prenatal services, delivery and 60 days of care afterward. If the costs come in below that amount, the medical practice gets to keep some of the savings. (Hospitals aren’t a part of this contract; the insurer pays them separately for their services.)

“We’ve always been taught to take care of patients as if they were our mothers and our daughters,” says Feltz, who also leads a coalition of obstetricians called the U.S. Women’s Health Alliance that advocates for high-quality, affordable care. “But now we have to take care of our patients as if they were our mothers and our daughters — and as if it was our money.”

This new program, announced in May, is a first step by the insurer to bundle physician payments for maternity care into a single flat fee that covers all care and procedures. A handful of insurers and state Medicaid programs are experimenting with similar models, sometimes incorporating hospitals and other health providers as well.

By moving from paying for maternity care in a piecemeal way to relying on bundled payments, insurers and doctors say they hope to cut costs and improve the quality of care for pregnant women.

But even fans of such a model acknowledge there are still significant obstacles to be worked out before this sort of flat-fee system could be implemented broadly.

The payment model is relatively new and still rare in maternity care; its structure can differ by insurer. Some insurers could pay a single amount to one doctor, who then uses part of it to cover hospital care. Other plans opt to cut a separate contract with the hospital. Insurers also vary in whether they make the lump sum payment before or after patients receive services. And the length of care, eligibility and services included in the bundle also vary.

In addition to, perhaps, reducing the overall cost of maternity care, the lump sums are seen by doctors and insurers as a possible way to improve health outcomes, including driving down the number of unnecessary cesarean sections in the United States.

About one-third of all deliveries in the U.S. occur via C-section, even though the World Health Organization estimates they are medically required in only 10% to 15% of births. The ratio of C-sections to live births varies dramatically among individual hospitals.

These surgeries can increase the risk of infections or other medical problems for the mother and baby. And they are more expensive than a vaginal delivery.

“The way we’ve been doing things is just not justifiable,” says David Lansky, a senior adviser at the Pacific Business Group on Health, a San Francisco-based coalition of private and public organizations that collectively purchase health care for 10 million Americans.

“The shift we’re talking about,” Lansky says, “is to say, ‘Someone is accountable for all the care that needs to be provided to support a family through this experience.’ “

Already, in traditional coverage, insurance payments for some women are delivered as bundled payments for some portions of their prenatal care, says Suzanne Delbanco, executive director of Catalyst for Payment Reform, a nonprofit organization that advises employers and other organizations that buy health coverage. However, she says, the new bundled payment models are different because insurers are adding quality measures that increase accountability to the bundle, as well as additional services such as labor and delivery.

Patients generally are not even aware their care is being handled under a bundled payment.

UnitedHealthcare, which announced its program in May, began testing the option with Feltz’s practice and another in Texas. The insurer says it hopes to expand to as many as 20 practices by the end of the year. Cigna and Humana are also piloting bundled maternity care programs. A few Medicaid programs, including those in Arkansas, Ohio and Tennessee, have experimented with it, too, in recent years.

Expanding the rarely used model to include maternity care could represent a major shift in health care finance. Births were the most common reason for hospitalizations among U.S. patients discharged in 2016, according to government data.

“Maternity care is kind of the sleeper of health care services,” says Dr. Neel Shah, an assistant professor of obstetrics, gynecology and reproductive biology at Harvard Medical School.

The change in payments is being made as the quality of maternity care in the United States comes under renewed scrutiny. An estimated 700 women in the U.S. die each year because of pregnancy-related complications, the federal Centers for Disease Control and Prevention reports. The rate of deaths in the U.S. is worse than in many other affluent countries, NPR and ProPublica reported in 2017.

C-sections also cost more than vaginal deliveries. In the Denver area, for instance, the average vaginal delivery costs $7,716 while the average C-section costs $14,274, according to 2019 data from the Health Care Cost Institute. On average, commercial and Medicaid insurers pay 50% more for C-sections than for vaginal deliveries, according to a 2013 report by Truven Health Analytics, a health industry consulting group.

Lansky’s group provided funding, data and oversight in 2014 for a project to test bundled payments for births in a variety of Southern California hospitals. According to their report, the rate of C-sections in first-time, low-risk pregnancies dropped by nearly 20% in less than one year among the first three participating hospitals.

However, some of the bundled-payment models have fallen short of aspirations. Tennessee saved money in 2017 after adopting the payment model for Medicaid beneficiaries. But the rate of C-sections remained unchanged, according to a report by the Medicaid and CHIP Payment and Access Commission, a nonpartisan advisory group for Congress.

In Ohio, where the Medicaid program covered complicated pregnancies as well as those that were low-risk, bundling payments into a lump sum for OB-GYNs cost the state more than expected, the advisory group found.

Bundling raises other concerns, too. Because some bundled-payment programs assign the total cost of care to a single physician, the financial burden falls on that physician. Dr. Lisa Hollier, the immediate past president of the American College of Obstetricians and Gynecologists, is concerned that these models may discourage team-based care.

If the physician providing prenatal care overlooks a problem that a different doctor must treat during delivery, for example, it wouldn’t be fair for the OB-GYN delivering the baby to bear the financial burden, Hollier says.

How payers define a low-risk pregnancy is also unclear, she says. If the target price for the suite of services in the model is not risk-adjusted for the cost of treating conditions like gestational diabetes, she says, doctors could be penalized for treating these patients.

Gestational diabetes occurs in up to 10% of pregnancies in the U.S. annually, according to the CDC, and patients with the condition need additional tests, checkups and insulin.

Julianne Pantaleone, national director of bundled payments and strategy at UnitedHealthcare, says that as the insurer works through its pilot program, it will cover the cost of physician care beyond the initial budget.

The lack of robust data systems built for handling bundled payments also poses a potential barrier for some medical practices, says Blair Barrett Dudley, a senior manager at the Pacific Business Group on Health.

Insurers and doctors need real-time data to ensure they are meeting the model’s quality measures, she says. However, these information banks are expensive to build, and many of the existing ones aren’t designed to handle this payment structure.

Feltz agrees that getting such data will be imperative to a successful bundled payment program. Without the information, he says, “it’s like launching a ship and not knowing where it’s going to go.”

Kaiser Health News is a nonprofit, editorially independent program of the Kaiser Family Foundation. KHN is not affiliated with Kaiser Permanente.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}